Raising Capital for Deep Tech in Australia: How to Turn Complex Science Into Funded Companies

- Steve Torso

- 10 hours ago

- 10 min read

Here's a pattern I've seen hundreds of times. A deep tech founder walks into a room with a breakthrough in AI, quantum computing, robotics, or space technology. The science is genuinely world-class. The team includes PhDs from Australia's top research institutions. The IP is defensible. The market opportunity is massive.

They present. The investors nod politely. Nobody writes a cheque.

The problem is rarely the technology. It's that the founder explained what the technology does without ever explaining who it's for, what changes for that customer, and why an investor should care right now.

After 17 years inside the private capital ecosystem, I can tell you that the gap between brilliant deep tech and funded deep tech in Australia is not a capital gap. It's a translation gap. And the founders who learn to close it are the ones building the companies that matter.

Here's what the data says about raising capital for deep tech in Australia in 2026.

Deep Tech Is the Sector Investors Want Most

From our 2026 Wholesale Investor Survey of more than 100 active private market participants, 37% of investors plan to actively deploy into Deep Tech (AI, Robotics, Quantum, Space) in 2026.

That makes it the second-highest sector by investor interest, behind only Technology broadly (38%). It sits ahead of Private Equity (34%), Renewables (32%), HealthTech (31%), and Life Sciences (30%).

Separately, the State of Australian Startup Funding report for 2025 found that the most cited sectors to watch in 2026 were Artificial Intelligence (71%), Hardware/Robotics/IoT (35%), and Deep Tech (33%). Australian equity funding reached $503 million across 25 rounds in the first two months of 2026 alone, up 27% from the same period in 2025, driven heavily by AI, climate tech, and deep tech sectors.

The appetite is strong and growing. But appetite and access are different things. Most deep tech founders aren't converting investor interest into committed capital because they're speaking a language investors don't understand.

Who Is Actually Investing in Australian Deep Tech?

This is where most deep tech founders miscalibrate their entire approach.

They assume their investors will be specialist deep tech VCs who understand transformer architectures, quantum error correction, or orbital mechanics. Some will be. But they represent a small fraction of the available capital.

Our survey data shows that 44% of active investors are sophisticated or wholesale individuals. Another 25% are founder-investors. Nearly 70% of the active investor base is making personal, conviction-driven decisions without a formal investment committee or a PhD in physics.

49% of these investors have backgrounds in financial services and banking. 31% have sales and go-to-market expertise. 27% come from manufacturing and industrial backgrounds. 29% from energy and infrastructure.

This is your actual investor base. They understand business. They understand markets. They understand operational execution. What they don't understand, and shouldn't be expected to understand, is the technical nuance of your deep tech stack.

The founders who raise successfully in Australian deep tech are the ones who meet these investors where they are: with commercial language, industry context, and clear articulation of who pays for this and why.

The Translation Problem: Why Great Technology Doesn't Raise Capital

I recently worked with a deep-tech company that had genuinely impressive technology. When they presented, they explained the engineering, the architecture, and the technical differentiation. What they never explained was who the end customer actually is and how the technology benefits that customer in practical, measurable terms.

This is the single most common failure in deep tech fundraising in Australia. Founders fall in love with describing what the technology does and forget to describe what the technology does for someone.

The fix is what I call grounding the technology in sectors investors already understand.

Australia has dominant industries that every investor in the country knows: mining, agriculture, energy, defence, construction, and healthcare. When a deep tech founder can ground their technology in one of these sectors, the investor doesn't need to understand the engineering. They need to understand the problem and the outcome.

Compare these two pitches:

"We're building computer vision models using transformer architecture with proprietary training data for industrial applications."

versus

"We help mining companies detect equipment failures 72 hours before they happen. Each failure costs $2 million in downtime. We charge $500,000 per year per site. BHP is in pilot."

Same company. Same technology. One pitch gets polite nods. The other gets a follow-up meeting.

The technology is the engine. The customer outcome is the story. In deep tech fundraising, the story is what raises the money.

What Deep Tech Investors Care About Before the First Meeting

Our survey identified the trust signals that matter most when investors decide whether to engage with a direct company opportunity. For deep tech, three of these are particularly important.

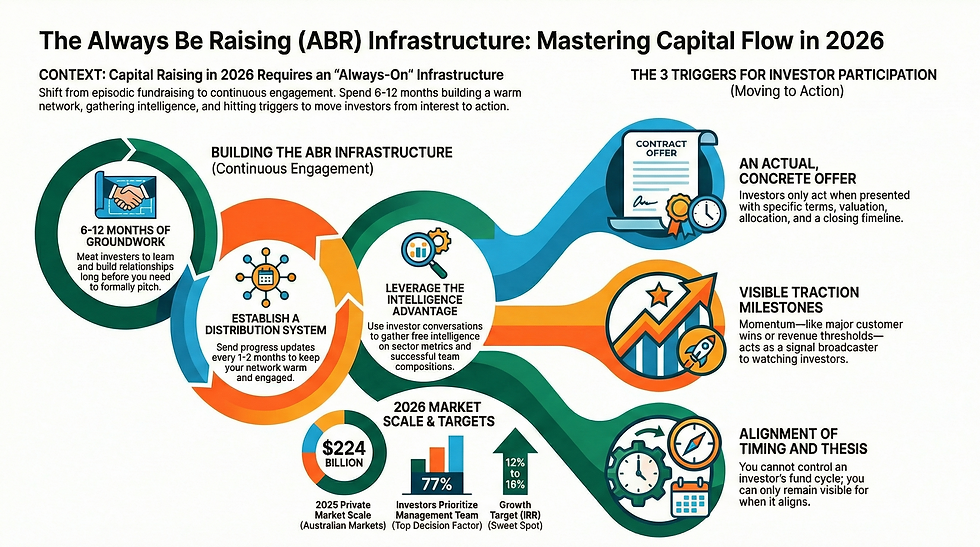

Management track record: 77%. The number one factor by a wide margin. In deep tech, this means something specific. Investors aren't just looking for previous exits. They're looking for evidence that the team can commercialise complex technology. Can they build a product from a research prototype? Can they sell to enterprise customers? Can they navigate the regulatory and procurement cycles of large industries?

If your team is entirely academic, this is a red flag for most investors. Compensate by bringing in commercial co-founders, advisory board members with industry exits, or operational leaders from the sectors you're targeting.

Competitive moat: 55%. This is where deep tech has a natural advantage, and most founders undersell it. Patents, proprietary datasets, years of R&D that competitors can't replicate, relationships with research institutions, government clearances. These barriers to entry are exactly what investors want to see.

But you have to articulate the moat in investor language. "Our technology uses a novel approach to quantum error correction" is a feature. "We hold 14 patents, it took us 7 years and $12 million of government-funded research to develop this capability, and the nearest competitor is 3 years behind" is a moat.

Commercial traction: 56%. In deep tech, traction doesn't always mean revenue. It means evidence of commercial demand. Pilot agreements with enterprise customers. Letters of intent. Government contracts. Industry partnerships. Paid proof-of-concept engagements.

The deep tech founders who struggle to raise are the ones who have been in the lab for five years with zero commercial validation. The ones who raise are the ones who found one customer early, even if the product is imperfect, and can show that someone is willing to pay for what they're building.

Making Deep Tech Relatable: The Humanisation Problem

In biotech, the humanisation of science is emotional. You connect with the patient. In deep tech, the humanisation is contextual. You connect with the industry, the end user, and the tangible outcome.

Most deep tech founders think their technology is self-evidently important. It rarely is, to anyone outside their field.

Our 2026 Investor Survey asked investors about problems or causes they have a deep personal conviction about. 42% cited AI and its exponential potential. 33% cited the future of finance. 34% cited food security and agriculture. 21% cited climate change and sustainability.

These conviction areas map directly onto deep tech applications. But the founder has to build the bridge.

An AI founder building autonomous agricultural systems needs to connect with the 34% of investors who care about food security. Not by explaining neural network architectures, but by explaining how Australian farmers lose $3 billion annually to crop disease that could be detected 14 days earlier with the right sensing technology. Suddenly, the investor isn't evaluating AI complexity. They're evaluating a solution to a problem they care about, in an industry they understand.

A quantum computing founder shouldn't lead with qubit counts. They should lead with what quantum simulation means for drug discovery timelines, materials science, or financial risk modelling. Ground the technology in the outcome, and the investor gets it.

The best deep tech founders I've watched raise capital use what I'd call the "three sentence bridge": one sentence on the problem (in a known industry), one sentence on what changes (the outcome), and one sentence on why only this technology can deliver it. The technology comes third, not first.

The Government Tailwind Most Founders Underutilise

Australia has committed extraordinary government support to deep tech, yet most founders either don't know about it or fail to communicate it effectively to investors.

The $15 billion National Reconstruction Fund has earmarked $1 billion specifically for critical technologies, including AI, robotics, and quantum. The National Quantum Strategy, backed by $60 million in direct funding, aims to position Australia as a global quantum leader by 2030. The $470 million investment in PsiQuantum signals the scale of government ambition.

The $36 million Critical Technologies Challenge Program is specifically accelerating the commercialisation of quantum technologies. The $3.4 billion Advanced Strategic Capabilities Accelerator targets defence applications for deep tech. And Australia's $1.6 billion Economic Accelerator funds translation and commercialisation in national priority areas.

The R&D Tax Incentive provides a 43.5% refundable offset on eligible R&D expenditure for companies with a turnover of $20 million or less. For deep tech companies where R&D is the primary activity, this materially extends runway and reduces investor risk.

AUKUS Pillar 2 has identified quantum, AI, and advanced cyber as priority capability areas, with eased export controls making it easier for Australian companies to collaborate with US and UK defence and intelligence partners.

For investors, government backing does two things. First, it de-risks the technology. If the Australian Government is investing billions in this sector, the market validation signal is strong.

Second, it creates customer pathways. Defence, infrastructure, and government procurement become accessible markets for deep tech companies aligned with national priorities.

The founders who raise well communicate this clearly: "We're building in a sector where the Australian Government has committed $1 billion through the National Reconstruction Fund. Our technology aligns with the List of Critical Technologies in the National Interest. And our first customer pipeline includes two defence procurement programmes."

That's a fundamentally different conversation than "we're building cool AI."

Deal Structures for Deep Tech

Deep tech timelines are longer than SaaS or consumer companies. The path from lab to revenue can take years. This affects how you should structure your raise.

Our survey found that 62% of investors prefer priced equity rounds. In deep tech, this means you need a defensible valuation methodology even at the pre-revenue stage. IP valuation, comparable transactions, and the cost-to-replicate approach are all relevant.

45% of investors target the Series A/B stage (proven traction, scaling). But 38% are willing to invest at seed and pre-revenue. The deep tech opportunity sits at the intersection: investors who understand that deep tech requires early capital but want to see evidence of commercial potential, not just research output.

47% of investors told us their preferred liquidity horizon is 3 to 5 years. Deep tech timelines often stretch to 5 to 7 years or longer. This is a friction point. The founders who address it directly, by showing interim value-creation milestones (licensing deals, government contracts, strategic partnerships) that don't depend on a full exit, have a significant advantage.

43% of investors write first cheques between $25,000 and $100,000. Don't lock out the majority of your investor base with artificially high minimums. Structure your round to allow sophisticated individuals to participate alongside institutional investors.

The Communication Cadence That Builds Confidence

Deep tech has a unique communication challenge. Milestones are infrequent. Technical progress is hard to explain. And the gap between "we're making progress" and "we have a product" can feel endless to investors.

From our survey, 18% of investors cited founders disappearing after investment as a major frustration. 44% said too much noise, not enough signal. In deep tech, both problems manifest simultaneously: founders either go quiet because they don't think they have anything to report, or they send dense technical updates that investors can't interpret.

The solution is structured, regular communication that translates technical progress into a commercial context.

Monthly updates. Every month. Even when there's nothing dramatic to report. The update answers three questions: what progress we made, what it means for the commercial timeline, and what the next milestone is.

"This month, we achieved a 40% improvement in processing speed on our quantum simulation benchmark. This matters because it moves us closer to the performance threshold required by our first enterprise customer. Next milestone: live pilot deployment in Q3."

That's a signal. An investor reads that in 90 seconds and feels confident that progress is being made toward a commercial outcome.

99% of investors prefer to receive deal opportunities and updates via email. Not Slack, not a platform dashboard. Email. Build your investor communication infrastructure around it.

The Geographic Strategy

73% of investors in our survey focus on Australia. But 27% also target the US, and 20% look at Singapore and Southeast Asia.

For deep tech, the US market matters enormously. US defence procurement, Silicon Valley strategic acquirers, and US-based deep tech VCs represent the most likely exit pathways for many Australian deep tech companies.

The AUKUS partnership is opening new doors. Australian quantum companies like Silicon Quantum Computing and Diraq have been selected by DARPA for advanced development programmes. Australian space companies like Fleet Space Technologies are accessing NASA supply chains. These are not just technical validations. They are commercial pathways.

The founders who position their companies as globally competitive with an Australian R&D cost advantage, rather than "Australian deep tech companies," raise more effectively. Your technology competes globally. Your cost base is local. That's an advantage worth articulating.

What the Best Deep Tech Founders Do Differently: A Summary

Ground the technology in known industries. Mining, agriculture, defence, energy, healthcare. If an investor can't picture who buys this, they won't invest.

Lead with the outcome, not the engineering. The three-sentence bridge: problem, outcome, then technology. In that order.

Build the team for commercialisation, not just research. 77% of investors say track record is the top factor. If your team is all PhDs with no commercial experience, fix that before you raise.

Quantify the moat. Don't just say you have IP. Say you have 14 patents, 7 years of R&D, $12 million in prior government investment, and a 3-year lead on competitors.

Use government backing as a credibility signal. $1 billion NRF allocation to critical tech, AUKUS alignment, DARPA selection. These signals de-risk the investment for private investors.

Communicate monthly in commercial language. Translate technical milestones into progress toward revenue, customers, and exit. Never send a technical update without commercial context.

Address the long timeline directly. Show interim value-creation milestones (licensing, government contracts, pilots) that provide confidence even before a full exit.

Price your round clearly and keep minimums accessible. 62% want priced equity. 43% write first cheques under $100,000.

The Bigger Picture

Australia is building a genuine deep tech ecosystem. Government backing is substantial and growing. Research institutions are world-class. The investor appetite is real, with 37% of active investors targeting the sector. And cross-border pathways through AUKUS and strategic partnerships are creating commercial opportunities that didn't exist five years ago.

But the gap between research excellence and commercial success remains wide. Not because the technology isn't good enough. The engagement between founders and capital is still driven by fragmented communication, inconsistent updates, and founders who can't translate what they're building into a language investors understand and trust.

The deep tech founders who will define Australia's next wave of globally competitive companies won't just be the best engineers. They'll be the ones who build the bridge between complex science and committed capital. Between what the technology can do and what it means for the people and industries it serves.

That bridge is the most important piece of infrastructure in Australian deep tech. And right now, almost nobody is building it.

Steve Torso is the founder of Wholesale Investor, Australia's largest sophisticated investor network with over 45,000 investors. The data cited are from the 2026 Wholesale Investor Survey of active private market participants. For broader insights on raising capital in Australia, read our complete 2026 investor data analysis. For sector-specific guidance on biotech and life sciences, see our life sciences capital raising guide.